Company Update / Coal / IJ / Click here for full PDF version

Author(s): Reggie Parengkuan ;Ryan Winipta

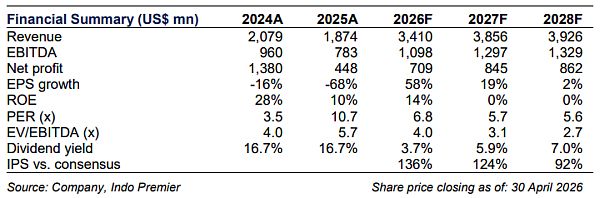

- reported 1Q26 NP of US$128mn (-12% yoy) which came optically below ours but in-line with consensus FY26F estimates at 18/25%.

- is only expected to start recording aluminum sales in 2H26F and thus NP will only start catching up by then.

- We maintain our NP estimates for now and maintain Buy at unchanged TP of Rp3,600.

1Q26 NP declined from lower sales volumes; but was in-line to cons

1Q26 NP declined to US$128mn (-12% qoq/+23% yoy) on the back of lower coking coal sales volume (-22% qoq), in addition to lower SIS volume and margin (-13/-22% qoq). 1Q26 NP came optically below ours and in-line with consensus FY26F estimates at 18/25% as 's aluminium plant is only expected to record sales in 2H26F. Below operating line, income from associates surged to US$25mn (+78% qoq), thanks to improving BPI earnings.

: higher cash margin was offset by lower sales volume

1Q26 production declined 14% qoq to 1.7Mt on higher rainfall, while sales was worse off at 1.5Mt (-22% qoq), likely due to logistical constraints. ASP rose to US$182/t (+15% qoq), in-line with higher coking coal price. At the same time, cash cost rose to US$94/t (+10% qoq) on the back of higher SR of 3.6x (+4% qoq), mining cost per ton (+13% qoq) from rising fuel price (Brent: +17% qoq), and higher royalty rate of 15% (4Q25: 12%). Nonetheless, cash margin still rose to US$88/t (+17% qoq). Overall, sales and SR were in-line with 's FY26F guidance (link).

SIS: cash margin declined on lower sales volume

SIS coal transport and OB volume declined to 15.3Mt/43.9mbcm (-9/-15% qoq) on the back of higher rainfall. As a result, cash cost rose to US$2.3/t (+18% qoq) from underutilization, while mining fee remained relatively flattish at US$3.3/t (+2% qoq). As a result, cash margin declined to US$1/t (-22% qoq).

Maintain our Buy rating at unchanged SOTP -based TP of Rp3,600/sh

We maintain our NP estimates for now as we await clarity from management and maintain our Buy rating at unchanged SOTP -based TP of Rp3,600/sh. We continue to believe 's intrinsic value remains underappreciated, with IPS TP excl. green business at Rp3,000/sh. Key downside risks are lower than expected coking coal price, delays in aluminium ramp up or future project expansion, capex overrun, B50 implementation, and rising fuel cost from Middle East tension.

Sumber : IPS