Company Update / Coal / IJ / Click here for full PDF version

Author(s): Reggie Parengkuan ; Ryan Winipta

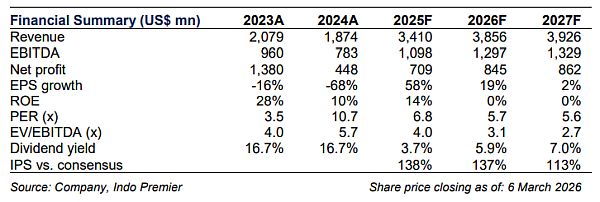

- reported FY25 NP of US$448mn (-73% yoy) which came in-line with ours but above consensus FY25F estimates at 99/120%.

- 4Q25 NP rose to US$146mn (+15% qoq); strong volume/margin (+24/+17% qoq) was partly offset by soft SIS and ECL provision.

- We upgrade our FY26/27F NP estimates by 31/42%, reflecting higher coking coal price assumption; reiterate Buy at higher TP of Rp3,600.

Solid 4Q25 NP on stellar volume and margin; FY25 above cons

reported FY25 NP of US$448mn (-73% yoy), in-line with ours (at 99%) but above consensus FY25F forecast (at 120%), mainly due to lower-than-expected opex (50% consensus). On quarterly basis, 4Q25 NP rose to US$146mn (+15% qoq), driven by a surge in sales volume and cash margin (+24/+17% qoq), but was partly offset by soft SIS volumes and margin (-14/-2% qoq), in addition to 's US$34mn ECL allowance. Below operating line, income from associates more than doubled to US$14mn supported by improving performance at BPI.

: sales volume and cash margin surged

4Q25 production volume remained stable at 2Mt in 4Q25 (+2% qoq), while sales volume surged to 1.9Mt (+21% qoq) following easing logistical constraints. FY25 sales volume of 6.3Mt (+12% yoy) exceeded 's FY25F guidance (at 105%). ASP rose to US$159/t in 4Q25 (+7% qoq), in-line with coking coal index (+8% qoq). Meanwhile, cash cost declined to US$85/t (-1% qoq) on the back of lower SR of 3.5x (-8% qoq), lifting cash margin to US$74/t (+17% qoq). ( result note).

SIS: NP dropped on lower volumes

SIS coal transport and OB volume declined to 16.7Mt/51.4mbcm in 4Q25 (-4/-16% qoq), likely due to seasonality. As a result, cash cost rose to US$1.9/t (+2% qoq) due to operating leverage and cash margin declined to US$1.3/t (-2% qoq). SIS 4Q25 NP declined to US$26mn (-57% qoq).

Reiterate our Buy rating at higher SOTP -based TP of Rp3,600/sh

We upgrade our FY26/27F NP estimates by 31/42% to mainly reflect higher coking coal price assumption of US$220/t (from US$200/t previously) and incorporating 's aluminium project into our model. Consequently, we upgrade our SOTP -based TP to Rp3,600/sh (from Rp2,800/sh previously) and reiterate our Buy rating. We continue to believe 's intrinsic value remains underappreciated, with IPS TP excl. green business at Rp3,000/sh. Key downside risks are lower than expected coking coal price, delays in aluminium ramp up or future project expansion, and capex overrun.

Sumber : IPS