Company Update / Metals / IJ / Click here for full PDF version

Author(s): Ryan Winipta ;Reggie Parengkuan

- purchased 30% stake in Jiu Long Metal Industry ( JLMI , 28ktpa NPI smelter) for US$103mn while Tsingshan retains remaining stake.

- In exchange for the minority stake in JLMI , received nickel ore offtake agreement of 3mn wmt ore p.a. for the next three years.

- We think the impact to P&L shall be muted in the short-term, but the transaction is necessary in order to retain Gag Nikel license (CCoW).

Overview on 30% stake purchase in JLMI ; 3-4 years payback period

via its 100% wholly-owned subsidiary, PT Gag Nikel ( PTGN ) is set to purchase 30% minority stake in Jiu Long Metal Industry - 28ktpa NPI smelter located in Weda Bay area ( IWIP ) while the remaining 70% stake is retained by Tsingshan. The smelter has been operating since 2020 and has a similar cash cost to other smelter in IWIP which is around US$10-11k/t based on our checks. Hence, our calculation indicates 3-4 years payback period from the investment if we take into account free-cash flow (FCF) from the nickel ore sales (Fig. 2).

Limited P&L impact from ore offtake in the ST, FY25F at soonest

By doing 30% stake purchase, obtained an ore supply agreement to JLMI smelter of around 3mn wmt for the next 3-years which could be further extended by the end of three years. However, since Gag Nikel itself has been supplying 3mn wmt ore p.a. to non- JLMI based on the latest run-rate, net volume impact shall be limited as these 3mn wmt ore would only be re-allocated from other 3rdparty to newly-purchased JLMI . However, mentioned that it could raise its volume by addl. 1mn ore, albeit subject to RKAB approval in FY25F, on top of the aforementioned volume.

PT Gag Nikel ( PTGN ) CCoW's downstream requirement is met

We think long-term impact from the transaction is a positiveas Gag Nikel is one of the last nickel mine with contract of work (CCoW) license and needs to be converted to IUPK at the time of expiry in 2047 which will require an investment into downstream project. The investment into JLMI did meet the downstream requirement, eliminating further potential capex spending for greenfield project. Greenfield project could've yielded negative NPV, owing to low NPI profitability, absence of tax holiday, and 's track-record in P3FH's 13.5ktpa FeNi plant (6-8 years completion vs. 1-2 years typically).

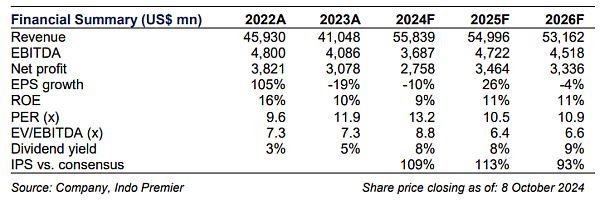

Maintain Buy rating with an unchanged TP of Rp1,750/share

We fine-tuned our FY24F/25F/26F NP forecast by +3%/+1%/+1% to take into account recent development in 3Q24F, c.30% stake purchase & ore offtake agreement. Our TP and Buy rating are kept unchanged given limited change in our NP forecast, is currently trading at 13x FY24F P/E. Downside risks are execution & operational risk from the ore offtake agreement.

Sumber : IPS