Company Update / Banks / IJ / Click here for full PDF version

Author(s): Jovent Muliadi ;Axel Azriel

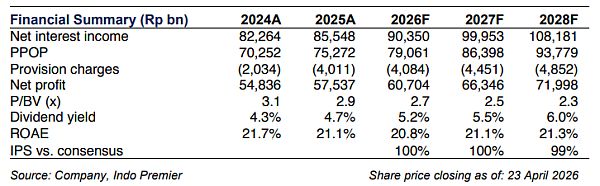

- 1Q26 net profit of Rp14.7tr (+4% yoy) came in-line. PPOP was moderate (+5% yoy) amid flat NII. CoC of 60bp was above guidance of 40-50bp.

- NIM fell -40bp yoy from lower asset yield. Deposit grew +8% yoy from solid (+11% yoy) while loan growth came modest at +6% yoy.

- Both NPL/LAR slightly rose on qoq basis to 1.8%/5.1%. We maintain Buy as drop in share price has reflected the slower growth expectation.

1Q26 results: moderate PPOP amid flattish NII while CoC came higher

recorded 1Q26 net profit of Rp14.7tr (+4% yoy/qoq) was in-line with our/consensus FY26F at 24%. PPOP was moderate at +5% yoy amid flat NII, despite robust non-II (+16% yoy). CIR improved to 27% vs. 29% in 1Q25. Provisions grew +20% yoy (+152% qoq), leading to higher CoC of 60bp (+10bp yoy/+20bp qoq).This was a tad higher than its guidance of 40-50bp and reflects its cautious stance within consumer and SME segments.

Decline in NIM from lower asset yield despite slight improvement in CoF

Consolidated NIM fell by -40bp yoy to 5.4% in 1Q26 (-20bp qoq), tracking at the lower-end FY26F guidance of 5.4-5.6%. This was attributed to lower asset yield (-45bp yoy) especially in the corporate segments (32% are linked with benchmark rate), though CoF has slightly improved by -10bp yoy. LDR stood at 74% (vs. 76% in 1Q25). Deposit grew +8% yoy driven by strong (+11% yoy), while TD still declined by -5% yoy. This led to improving ratio at 85% in 1Q26 vs. 83% in 1Q25.

Tepid loan growth dragged down by auto segment

Gross loan grew by +6% yoy (flat qoq), lower than its FY26F guidance of 8-10%. It was drivenprimarily by corporate (+9% yoy), followed by commercial (+6% yoy) and SME (+5% yoy), while consumer declined to -2% yoy, mostly dragged down by auto loan (-20% yoy) which offset modest growth in mortgage (+5% yoy) and personal loans (+7% yoy).

Slight qoq uptick on NPL/LAR

NPL experienced a slight qoq uptick at 1.8% in 1Q26 vs. 1.7% in 4Q25 (2.0% in 1Q25), along with higher LAR at 5.1% vs. 4.8% in 4Q25 (6.0% in 1Q25), sourced mostly from downgrades within the consumer and SME segments.Meanwhile, LAR coverage stood at 70% in 1Q26 vs.72/67% in4Q25/1Q25.

Maintain Buy on improving funding mix and attractive valuation

We maintain Buy on as drop in share price (-20% YTD) clearly reflect the slowing growth expectation. It currently trades at attractive valuation of 2.7x FY26F P/B and 13.0x P/E (vs. 10Y average of 3.8x and 20.9x). Risk is slower loan growth and further deterioration in asset quality.

Sumber : IPS