Company Update / Banks / IJ / Click here for full PDF version

Author(s): Jovent Muliadi ;Axel Azriel

- just announced that it has acquired Rp19.9tr of pension credit portfolio from .

- We think this shall be accretive for as the estimated loan yield stands at c.14-15% vs. current 's blended asset yield of 7.5-8%.

- Overall, we project the transaction to increase 's NIM by 15-17bp and FY26F EPS by 14-16% (half year impact). Risk is slow integration.

is acquiring Rp20tr of 's pension loan portfolio

just announced that it has acquired Rp19.9tr of pension loan from (5% of 's 1Q26 total loan book). As the transaction value stands at 54.1% of 's equity, it requires AGM approval which they already had since 23rdApril 2026. The takeover will be fully funded by third-party funds and it plans to increase the pension loan portfolio to Rp35-40tr eventually.

An accretive diversification strategy

Overall, the move is broadly in line with 's diversification strategy to raise the portion of non-housing exposure to 30% over the next five years. We view that pension loan is pretty well insulated against competition as not many banks are playing on this field, unlike payroll loan. Note that 's exposure to consumer (payroll) loan segment is very minimal at Rp8.5tr (2.1% of the total portfolio), and the acquisition shall increase consumer share to 7% of the total book.

Pension carries an attractive yield with resilient asset quality

We think that this transaction shall be accretive for as based on our channel check, the estimated loan yield of the acquired portfolio stands at c.14-15% vs. 's blended asset yield of 7.5-8% - we use the comparable of Bank Mandiri Taspen's pension loan yield of 13.6%. At the same time, it also has a very low CoC of <1% as pension's loan NPL usually hovers around 40-60bp. This is much lower than 's current CoC/NPL of 0.9/3.1% in 1Q26.

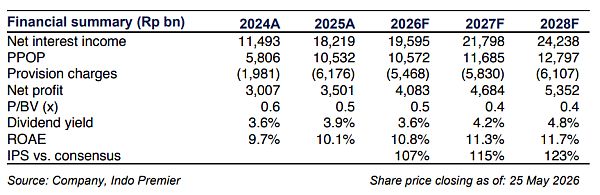

Maintain Buy as we expect positive impact to NIM/EPS

We project overall NIM to increase by c.15-17bp - under the assumption of half year impact, which translate to additional earnings of c.14-16% from our base FY26F case, all else being equal; 2027 impact will be bigger as it will have FY impact. Overall, we maintain Buy on amid better margin and asset quality outlook, as well as its strategic move to diversify its portfolio. It currently trades at an attractive valuation of 0.5x FY26F P/B and 4.8x P/E, compared to the 10Y average of 0.8x and 6.7x. Risk is slow operational integration.

Sumber : IPS