Sector Update / Banks / Click here for full PDF version

Author: Jovent Muliadi ; Axel Azriel

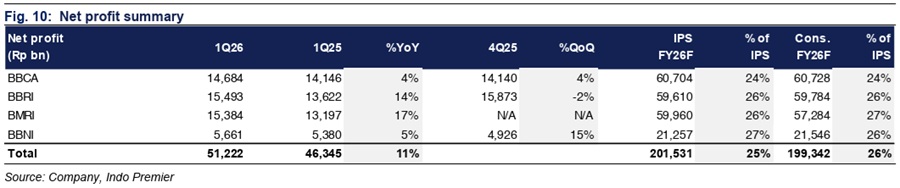

- Big 4 banks' net profit of Rp51.2tr in 1Q26 (+11% yoy) came in-line. PPOP grew +8% yoy, primarily led by /BMRI at +12/10% yoy.

- All banks recorded lower NIM except for (+20bp yoy), dragged by lower loan yield but was offset by improving CoF (-10bp to -65bp yoy).

- Asset quality was broadly stable but weakness in consumer was observed across banks. We maintain OW with and as our top picks.

In-line 1Q26 results across big 4 banks; /BMRI led the PPOP growth

Aggregate big 4 banks net profit of Rp51.2tr in 1Q26 (+11% yoy) was in-line at 25/26% of ours/cons, sourced from (+17% yoy) and (+14% yoy, due to low base effect in 1Q25 at -14% yoy). PPOP rose +8% yoy, led by (+12% yoy) and (+10% yoy). This was driven by decent NII (+9% yoy, with all SOE banks posted double-digit NII growth (11-12%) while came flattish yoy. Opex remained manageable at +8% yoy. Provision came flat amid drop in at -20% yoy and at -1% yoy, though and rose higher at +20/37% yoy amid their precautionary stances.

Overall NIM was dragged down by lower loan yield; but was partly offset by improving CoF

Most banks recorded NIM compression in 1Q26, led by (-40bp yoy), (-30bp yoy), and (-5bp yoy), except for which expanded by +20bp yoy. This was mostly dragged by lower loan yield (-30bp to -50bp yoy across big 4 banks), mainly due to lower reference rate within corporate segment and Agrinas loan for the SOEs. In terms of CoF, all big 4 banks already posted notable improvement, led by (-65bp yoy) and (-42bp yoy). All banks maintained their FY26F NIM guidance except for (from 4.6-4.8% to 4.5-4.7%) amid BSI deconsolidation & lower loan yield.

Robust loan expansion within SOE banks from Agrinas loans

Aggregate big 4 loans grew +14% yoy, with SOE banks posted robust growth of +14% to +20% yoy from Agrinas loan disbursement while was slower at +6% yoy. On the funding front, deposits grew solid by +17% yoy with balanced growth across TD (+22% yoy) and (+15% yoy - contributed primarily by CA at +23% yoy vs. SA of +8% yoy as Agrinas hasn't fully disbursed the loan).

Slight qoq LAR increase from consumer though overall NPL came stable

Overall asset quality was relatively stable for the big 4 banks. posted the qoq improvement in LAR (-48bp qoq), while slight hiccups were seen in (+7bp qoq), (+10bp qoq), and (+30bp qoq), sourced mostly from downgrade within the consumer and SME segments. In terms of NPL, only rose by +10bp qoq while came flat, down by -7bp qoq, and improved by -11bp qoq. CoC for all banks were still in-line with their guidance except for (higher at 60bp vs. guidance of 40-50bp).

Maintain OW from gradual CoF improvement and resilient asset quality

We maintain our OW stance on banks on the back of strong 1Q earnings and attractive valuation. The sector is currently trading at attractive valuation of 1.5x FY26F P/B and 8.2x P/E vs. 10Y avg of 2.2x and 14.4x. Our top picks are and . Key risk is prolonged geopolitical tensions which could lead to slower-than-expected loan growth and deterioration in asset quality.

Sumber : IPS