Sector Update / Banks / Click here for full PDF version

Author: Jovent Muliadi ;Axel Azriel

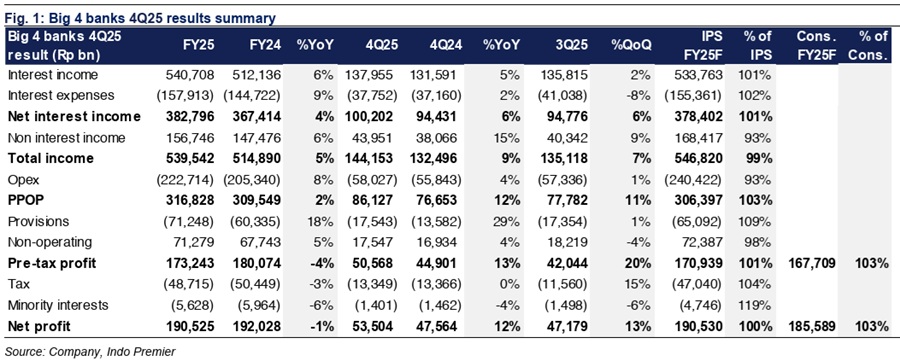

- Big 4 banks net profit of Rp191tr in FY25 (-1% yoy/+13% qoq in 4Q25) came in-line. /BBRI led the qoq expansion by +40%/+9% qoq.

- All banks recorded lower NIM in FY25 though /BBRI improved qoq from lower CoF. Jan26 results also indicated further CoF improvement.

- Asset quality improved across big 4 banks especially on LAR. We maintain OW and foresee +6% aggregate big 4 banks EPS growth in FY26F.

In-line FY25 results across big 4 banks; led the qoq improvement

Aggregate big 4 banks booked net profit of Rp191tr in FY25 (-1% yoy/+13% qoq), in-line at 100/103% of ours/cons. The qoq improvement was driven by (+40% qoq) and (+9% qoq), while both /BBNI fell -2% qoq. Aggregate PPOP grew at +2% yoy supported by NII growth (+4% yoy) and non-II (+6% yoy). Opex remained manageable at +8% yoy. Provision grew +18% yoy (+1% qoq), dragged by (+97% yoy) and (+21% yoy).

Jan26 bank-only results: robust earnings growth from /BMRI; was the strongest in terms of PPOP

In Jan26, aggregate big 4 bank-only earnings rose +22% yoy to Rp15.1tr, above our/cons FY26F consol growth estimates of +6%/5%. This was driven by (+85% yoy - due to low base effect in Jan25 at -58% yoy) and (+16% yoy), while /BBNI was modest at +6/3% yoy. Aggregate NIM fell -9bp yoy from lower asset yield (-33bp yoy) though CoF improved (-29bp yoy). Loan/deposit grew +13/16% yoy, bringing LDR to 87% (vs. 90% in Jan25).

Lower NIM from decline in loan yield though CoF improved in 4Q

All banks recorded NIM compression in FY25, led by (-40bp yoy), (-26bp yoy), and /BBRI (both by -10bp yoy). This was mostly dragged by lower loan yield from lower benchmark rate. On a positive note, /BBRI already posted NIM improvement on qoq basis (both by +30bp qoq in 4Q25), supported by lower CoF in 4Q25 at -47/-60bp qoq. Nevertheless, all banks prefer to be conservative by lowering their NIM guidance in FY26F by 10-40bp.

Loan expansion within SOE banks from village cooperative loans

Aggregate loans grew +12% yoy in FY25 with SOE banks recording robust growth of +12-16% yoy amid village cooperative loan disbursement in Dec25. In FY26F, SOE banks are anticipating slower loan growth (7-9%), while guides for slightly higher growth of 8-10% (6-8% in FY25). Deposit was robust at +17% yoy - but with caveat that village cooperative program money hasn't fully disbursed. Notably, outperformed in growth at +29% yoy.

Solid improvement in asset quality across all banks

Asset quality was improving across the big 4 in FY25. saw the largest LAR improvement at -180bp yoy, followed by (-110bp yoy), (-50bp yoy), and (-26bp yoy).Meanwhile,all big 4 banks guides for either flat or lower CoC in FY26F, except for which lift its guidance from 1% to 1-1.2% as it prefers to remain cautious on the retail segment.

Maintain OW from gradual CoF improvement and resilient asset quality

We maintained OW with /BMRI as our picks and foresee 6% aggregate EPS growth in FY26F, driven by improvement in CoF (as indicated in Jan26 results) and resilient asset quality. The sector currently trades at 1.8x FY26F P/B and 10.8x P/E vs. 10Y avg of 2.2x and 14.5x.Risks are fiscal & geopolitical noise which may bring more IDR volatility/higher bond yield.

Sumber : IPS