Sector Update / Banks / Click here for full PDF version

Author: Jovent Muliadi ;Axel Azriel

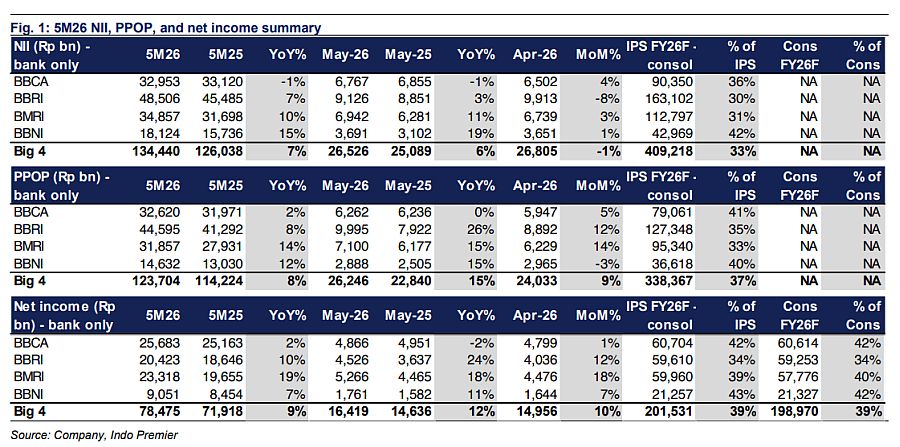

- Aggregate big 4 bank-only profit of Rp78.5tr in 5M26 (+9% yoy) came in-line. and led the PPOP growth at +14/12% yoy.

- Big 4 bank-only NIM declined by -21bp yoy to 5.1% from lower asset yield (-49bp yoy), though CoF has improved by -33bp yoy.

- We expect CoF to trend higher from Jun onwards which may further pressure NIM. Our top picks are now followed by .

5M26 bank-only results: in-line; and still led the PPOP growth

Aggregate big 4 bank-only earnings grew +9% yoy to Rp78.5tr in 5M26 (+10% mom), broadly in-line with our/cons FY26F consol growth estimates of +6/4%. Earnings growth was led by (+19% yoy) and (+10% yoy), whereas in terms of PPOP , was also the strongest at +14% yoy, followed by at +12% yoy. NIM fell -21bp yoy to 5.1% on lower asset yield (-49bp yoy) despite CoF improvement of -33bp yoy. Loan grew +15% yoy while deposit rose higher at +17% yoy, translating to lower LDR of 88% vs. 89% in 5M25.

: soft PPOP amid drop in NII while CoC was behind guidance

bank-only net profit of Rp25.7tr in 5M26 (+2% yoy/+1% mom) was in-line on consol basis (our estimate) at 42% ofour/cons FY26F. PPOP grew a modest +2% yoy as weak NII (-1% yoy) was offset by decent non-II (+8% yoy) and soft opex (+2% yoy). Provision fell -14% yoy (-628% mom), which brought CoC to 0.3% (-8bp yoy/-3bp mom), below guidance of 40-50bp. NIM eased to 5.5% (-47bp yoy) on lower asset yield (-49bp yoy), while CoF was stable. Loan grew +5% yoy vs. deposit of +9% yoy, bringing LDR to 77% vs. 80% in 5M25.

: beat in earnings supported by robust non-II

bank-only net profit reached Rp20.4tr in 5M26 (+10% yoy/+12% mom) and came above on consol basis(our estimate)at 44%/45% of IPS/cons. PPOP grew +8% yoy as robust non-II (+20% yoy) and decent NII (+7% yoy) offset higher opex (+13% yoy). Provision rose +8% yoy (+16% mom), bringing CoC to 3.4% (-4bp yoy/+6bp mom), still above guidance of 2.9-3.2%. NIM was stable at 6.4% as lower CoF (-68bp yoy) was offsetting the yield compression (-61bp yoy). Loan grew +12% yoy vs. deposit of +9% yoy, lifting LDR to 92% vs. 89% in 5M25.

: above from robust PPOP and lagging CoC

bank-only net profit of Rp23.3tr in 5M26 (+19% yoy/+18% mom) came above on consol basis(our estimate)at 44%/46% of IPS/cons FY26F, driven by robust PPOP (+14% yoy). Provision declined -16% yoy (flat mom), bringing CoC to 0.5% (-21bp yoy/+1bp mom), below guidance of 0.6-0.8% which we expect to catch-up in 2H. NIM eased to 4.2% (-21bp yoy) as lower asset yield (-58bp yoy) outweighed CoF improvement (-43bp yoy). Loan grew +21% yoy vs. deposit of +22% yoy, translating to LDR of 92% vs. 93% in 5M25.

: robust PPOP was supported by both NII and non-II

bank-only net profit of Rp9.1tr in 5M26 (+7% yoy/mom) was in-line on consol basis(our estimate)at 43% of IPS/cons FY26F. PPOP came solid (+12% yoy), driven by both strong NII/non-II (+15/10% yoy). Provisions rose +31% yoy (-17% mom), lifting CoC to 1.1% (+12bp yoy/+1bp mom) and within guidance of 1.0-1.2%. NIM was stable at 3.7%, as both asset yield and CoF was relatively unchanged yoy. Loan grew +25% yoy while deposit expanded +33% yoy, resulting in lower LDR of 88% vs. 95% in 5M25.

Sumber : IPS