Sector Update / Banks / Click here for full PDF version

Author: Jovent Muliadi ;Axel Azriel

- We just came back from a roadshow and was quite surprised that foreign investor remained very bearish on Indonesia.

- There are 3 main concerns for investors: 1) PSO, 2) fiscal capacity and 3) MSCI .

- There isn't any major concern on the fundamental other than minor concern on loan growth/margin outlook. /BBNI/BBTN are our picks.

PSO loan was one of the key discussions

One of the most consistent concerns that we got is the PSO (public serviceobligation) by SOE banks. For instance, the question on the bank was: 1)is there any other program than village cooperative( KDMP - Rp210tr/4.0% of big 4 SOE loan) that requires significant liquidity, 2) in terms of the detail for KDMP loan,most were asking whether MoF will cover both principal and interest for KDMP loangiven thatthe interest burden is quite significant for each cooperative i.e. Rp143mn p.a. or c.Rp12mn/month which requires c.Rp200mn of revenue/month (assuming 6% EBITDA margin similar to ) to be just breakeven. 3) Lastly,bigger proportion of PSO loan may eventually dilute SOE banks' margin and incremental loan growth to private sector.

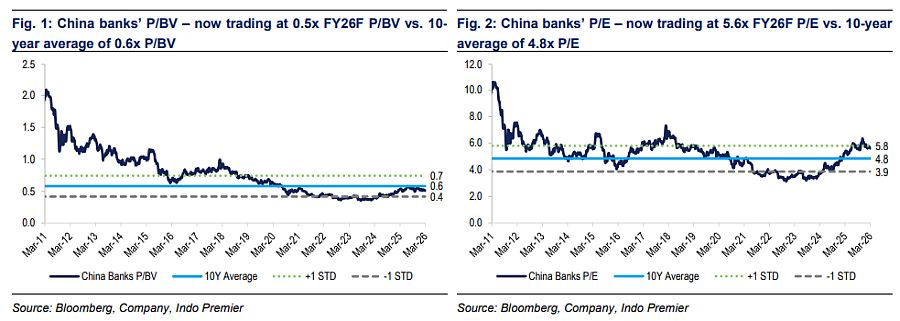

Investors are starting to compare the multiple of Indo's banks with China's banks

Given the aforementioned reasoning, some investors have started to compare the valuation of Indo's banks with China's banks. Currently China's banks trade at 0.5x P/B and 5.6x P/E (10Y average at 0.6x P/B and 4.8x P/E) vs. Indo's banks at 1.8x P/B and 10.1x P/E (10Y average at 2.2x P/B and 14.5x P/E) - a significant discount but bear in mind China's banks ROE at 9% currently (10Y average at 12%) vs. Indo's banks ROE at 18% (10Y average at 16%). We believe the comparison is unjustified given the difference in ROE and as we expect KDMP loan to be a one-off event.

Fiscal was another key concern

Another key concern was the fiscal situation in Indonesia which we have highlighted in our previous strategy note (link). Investors expect that themismatch between revenue (target is up by +14.4% yoy in FY26F from realization in FY25) and spending (target of +11.3% yoy in FY26F) may widen further this year of which our economist expects to reach Rp749tr deficit (-2.91% of GDP). This will eventually led to higher financing needs and bond yield which is negative for banks' valuation. It was also corroborated by the recent rating outlook downgrade by Moody's and Fitch.

Last concern is on potential MSCI downgrade to frontier market

Lastly, most investors remained concerned on the potential MSCI downgrade to frontier market given most of their mandate is emerging market (frontier market only constitute 1-2% EM AUM). Although most also believe that OJK and IDX have taken positive steps to address the MSCI concern.

Maintain OW with and as our picks

We remain positive on Indo banks given the earnings inflection thesis, valuation is at 6 years low (for P/B) and 12 years low (for P/E). /BBNI/BBTN are our picks as reflected in strong Jan26 earnings numbers (for /BBTN) while booked the strongest PPOP growth (+14% yoy).

Sumber : IPS