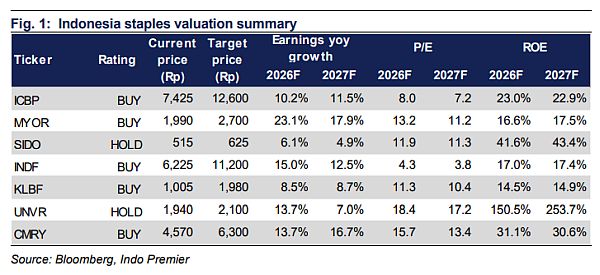

Sector Update / Consumer Staples / Click here for full PDF version

Author(s): Andrianto Saputra ;Nicholas Bryan

- Prolonged higher Brent oil price could eventually lead to higher several soft commodities prices such as sugar and API.

- is the most impacted from higher Brent oil prices as we estimate every 5% increase in raw material could reduce FY26F profit by -6.1%.

- We maintain Overweight amid tangible improvement in purchasing power.

Higher Brent oil price may lead to higher raw materials prices

Brent oil prices have increased significantly by 15.9% since the Middle East escalation on 28thFeb26 which may impact packaging costs for staples. Historically, higher Brent oil prices have indirectly impacted sugar prices (Fig. 4-5) as sugarcane material can be processed into either sugar or ethanol. Hence, higher Brent oil prices could incentive producers to allocate more sugarcane towards ethanol production, resulting in lower sugar supply and potentially higher sugar prices. Furthermore, sustained elevated Brent oil prices could also lead to higher Active Pharmaceutical Ingredient (API) prices, given energy and petrochemical linkages.

is the most impacted from prolonged higher Brent oil prices

We note that combined packaging, sugar and API contributed 15.9/2.6/18.1/19.4/16.5/16.7% of /ICBP/KLBF/UNVR/SIDO/CMRY's COGS . Our sensitivity analysis showed that every 5% increase in these raw material costs could decrease FY26F earnings by -6.1/-0.5/-4/-4.8/-0.4/-1.9% for /ICBP/KLBF/UNVR/SIDO/CMRY. To note, is the most impacted from a higher input cost due to its relatively lower NPM compared to its peers. Our conversation with staples companies suggest that they are currently monitoring the pass-through impact of higher Brent oil prices on raw materials before deciding whether to increase ASP.

/CMRY are the most impacted from USD/IDR appreciation

Within our coverage, we analysed consumer staples USD exposure (direct and indirect) in terms of costs and revenue (Fig. 2). In terms of costs, we note that /ICBP/KLBF/UNVR/SIDO/CMRY's 53/50/21/25/22/31% COGS are USD-linked. In terms of revenue, 37/26/6/3/3/0% of /ICBP/KLBF/UNVR/SIDO/CRMY's sales are USD-linked. We note, a higher /ICBP's USD-linked exposures are partly offset by their USD revenue contribution. Our sensitivity analysis showed that every 5% USD/IDR appreciation, it may reduce -2.7/-1.6/-2.4/-3.7/-0.8/-3.6% of /ICBP/KLBF/UNVR/SIDO/CMRY's FY26F earnings.

Maintain Overweight

Staples's valuation has dropped to 12.5x fwd. 12M PE (-1.7 s.d. from its 5yr mean), suggesting a limited downside. Moreover, our conversation with staples companies indicates that the sales have recovered since 4Q25F through Feb26, partly driven by government stimulus and MBG program. Overall, we maintain our OW for the sector amid a tangible purchasing power improvement since 4Q25F. Our pecking order is: >CMRY>>KLBF>>SIDO. Risk to our call: prolonged geopolitical tension and soft purchasing power.

Sumber : IPS