Company Update / Tobacco / IJ / Click here for full PDF version

Author(s): Andrianto Saputra ;Nicholas Bryan

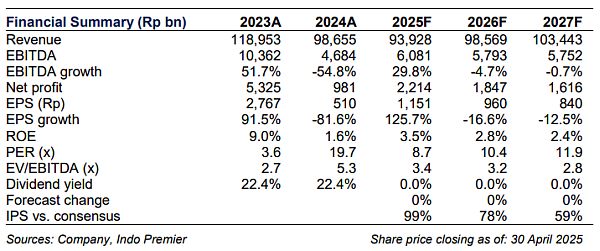

- 9M25 net profit of Rp1.1tr (+11.5% yoy) was above our/consensus estimate at 100/172% (vs. 5yr avg of 77%). 9M25 revenue was in-line.

- Strong 3Q25 earnings recovery was driven by GPM improvement of +153bps yoy and opex-to-sales improvement of +244bps yoy.

- Upgrade to BUY with a higher TP of Rp20,700/sh following our FY25/26F earnings upgrade of +82/100%.

9M25 earnings was above our and consensus estimate

posted 9M25 net profit of Rp1.1tr (+11.5% yoy), above our/consensus estimate at 100%/172% (vs. 5yr avg of 77%), supported by margin improvement at both gross profit and opex levels. 9M25 revenue of Rp67.3tr (-8.9% yoy) was in-line with our/consensus estimates at 76% (vs. 5yr avg of 75%). GPM declined to 9.4% (-54bps yoy), whileopex-to-salesimproved to 7.1% (-56bps yoy), resulting in a stable EBIT margin of 2.2% (+2bps yoy).

3Q25 revenue decline driven by weaker SKM and SKT sales

3Q25 revenue declined to Rp22.9tr (-3.8% yoy), attributed to soft SKM and SKT sales (-11.3%/-5.3% yoy). We estimate the revenue decline was volume-driven, as our channel checks indicate 3Q25 SKM ASP only increased +4.3% yoy. 3Q25 GPM improved to 11.0% (+153bps yoy), amid SKM ASP hikes (+4.3% yoy) and stable excise tax.Opex-to-salesimproved to 6.1% (-244bps yoy), mainly from lower A&P-to-sales ratio of 1.4% (-172bps yoy). Consequently, EBIT margin rose to 4.8% (+391bps yoy), driving a sharp rebound in net profit to Rp990bn (+1,384% yoy) with an NPM of 4.3% (vs. 0.3% in 3Q24).

FY25/26F earnings revised up by 82/100%

With the government maintaining a flat excise tax in FY26F (link tonote), we expect 's 3Q25 GPM of 11% to be sustained through FY26F. Continued opex efficiency is also expected, supported by a lower workforce (Fig. 3), as salary-to-sales dropped to 2.3% in 9M25 (vs. 2.6% in FY24). In sum, we raised our FY25/26F earnings forecasts by 82%/100% to reflect robust 3Q25 results..

Upgrade to BUY with TP of Rp20,700/sh

We upgrade to BUY with a TP of Rp20,700/sh, based on 11.0x FY26F PE (-0.5 s.d. from its 3yr mean). We also see sector upside as the Ministry of Finance intensifies enforcement against illegal cigarettes. Key risks to our call: softer sales volume than expected and higher penetration of illegal cigarettes.

Sumber : IPS