Company Update / Consumer Staples / IJ / Click here for full PDF version

Author(s): Andrianto Saputra ;Nicholas Bryan

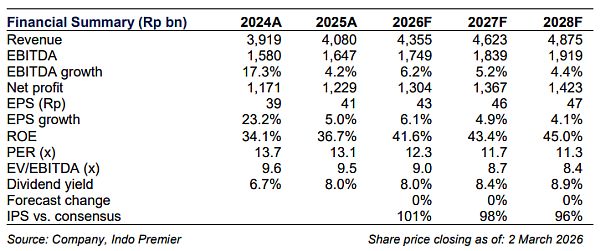

- FY25 net profit of Rp1.2tr (+5.0% yoy) was in-line with our/consensus estimate at 98/101%. FY25 revenue was also in-line

- 4Q25 sales growth of 4.5% yoy was driven by F&B sales growth of +34.4% yoy (vs. herbal's -5.7% yoy).

- Maintain our HOLD call with unchanged TP of Rp625/sh.

FY25 net profit was in-line with our/consensus estimate

booked FY25 net profit of Rp1.2tr (+5.0% yoy) and this was in-line with our/consensus estimate at 98/101%. FY25 revenue of Rp4.0tr (+4.1% yoy) was also in-line at 97/100% of our/consensus estimate. FY25 GPM declined to 58.0% (-74bps yoy), while opex to sales improved to 20.6% (-47bps yoy), resulting in EBIT margin of 37.3% (-27bps yoy). Overall, FY25 revenue/net profit growth of +4.1/+5.0% yoy was in-line with FY25 company guidance of +5.0% yoy.

4Q25 sales growth was driven by F&B segment

4Q25 revenue rose by +4.5% yoy to Rp1.4tr as robust F&B segment (+34.4% yoy) has fully offset the weakness herbal segment (-5.7% yoy). Soft Herbal segment sales growth of -5.7% yoy may indicate a higher inventory level at distributor level despite a last bite offer. We note that overall revenue growth of +4.5% yoy was attributed by related party distributor with sales growth of 7.3% yoy (vs. third-party's +1.3% yoy), suggesting a recovery in GT channels.

4Q25 opex improvement was being offset by GPM decline

4Q25 GPM declined to 60.6% (-235bps yoy) due to product mix change as herbal sales declined by -5.7% yoy (vs. F&B's +34.4% yoy) - (Fig. 1). Opex to sales ratio improved to 21.5% (-239bps yoy) amid lower A&P to sales ratio of -371bps yoy. As a result, EBIT margin stood at 39.1% (+4bps yoy). Overall, 4Q25 net profit stood at Rp411bn (+4.5% yoy) with a flat NPM of 30.4%.

Maintain our HOLD call with unchanged TP of Rp625/sh

We maintain our forecast as we await further details from the upcoming earnings call. In sum, we maintain our HOLD call with unchanged TP of Rp625/sh, based on 14.5x FY26F PE (-1.s.d from its 5yr mean). Key risk is soft purchasing power.

Sumber : IPS