Strategy Update / Click here for full PDF version

Author(s): Jovent Muliadi ;Anthony

- JCI dropped by 11% YTD (-12% mom) with total foreign outflow of Rp20tr in 2M25 (-Rp16tr alone in Feb25). Banks led the sell-off at -Rp15tr YTD.

- We have highlighted both domestic/external risks back in Nov24 (link), however, we think valuation clearly has priced-in most of the overhangs.

- Despite the attractive valuation, we remain cautious on domestic macro i.e. slower GDP growth, populist measure; and external factor (currency).

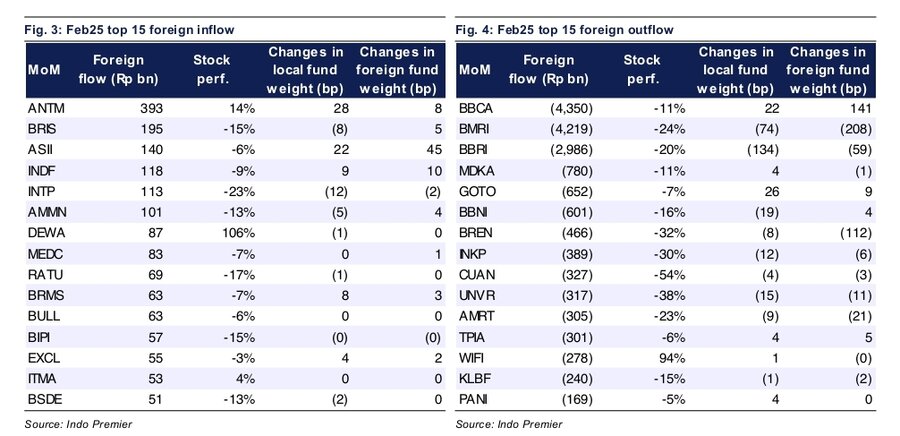

Banks has led the YTD outflow

JCI recorded an outflow of -Rp20tr in 2M25 with -Rp16tr in Feb alone. This was being led by banks at -Rp15tr YTD followed by tech (). This has resulted in -12% drop in JCI (-21% since Sep24) led by banks at -16% as of end Feb25 (-31% since Sep24). On stock level, led the outflow with -Rp7.2tr (-13% YTD), at -Rp4.2tr (-19% YTD) and at -Rp3tr (-18% YTD). We observed inflow mainly to /ANTM/INDF at c.Rp300bn each.

What has caused the sell-off?

We have highlighted several risks in our Nov24 note (link) which are: 1) risk on earnings revision (banks' earnings are being revised by average of xx%) and unattractive earnings growth (now at +1% for IPS universe/+3% for JCI), 2) uncertainty over Danantara, 3) currency from trade war and 4) short-term populist measures i.e. 3mn housing program, loan amnesty program, etc.

Most of the aforementioned risks have been priced-in with pace of sell-off is worse vs. 2015/2018

We think that most of the risks have been priced-in as JCI/LQ45 earnings have been revised by -4 to -5% % YTD to +3/4% ('s Jan25 results at -58% yoy have also setting the expectation very low). This has also been reflected in valuation with JCI/LQ45 PE has dropped to 11.8/10.2x as of end Feb25 from Sep24 of 14.5/12.9x. Worth noting that current sell-off magnitude of -28% (LQ45) is even steeper vs. 2015 at -23% (Yuan devaluation and start of the rate hike cycle) and 2018 at -17% (trade war and Fed rate hike). Current sell-off is only slightly better vs. Covid at -33%.

Valuation and fundamentals are already comparable to Covid level

Despite the steep correction, we think that current valuation is too cheap to ignore i.e. JCI/LQ45 FY25F P/E at 11.8/10.2x is comparable to Covid low average of 12.3/11.2x (2015/18 average at 13-14x for both JCI and LQ45). At the same time, if we look at the big 4 banks valuation i.e. P/E and P/B of 10.8x and 1.9x (SOE banks' 7.8x and 1.3x) is actually the lowest vs. previous sell-offs i.e. 2015/2018/2020 average of 13.9x and 1.9x.At the same time, pace of IDR depreciation of 9% (from Sep24 to Feb25) is already similar to 2015/18 (Covid at -13%). Whereas real yield spread of c.240bp is already the highest compared to 2015/18/20.

Domestic macro situation remained the biggest risk for now

Post earnings revisions, we turned bullish on financials (/BBRI) recently (link) as we think most of the overhangs/bad news has been priced-in. We also like selective consumer names (/ICBP/GOTO) as lower soft commodity price is a boon for staples. For commodity, we like /AADI/ANTM largely due to valuation reason.At this point, we think the biggest risks are on domestic macro side i.e. weak GDP growth/populist measure and seasonally 2Q represent the weakest point for Rupiah.

Sumber : IPS