Strategy Update / Click here for full PDF version

Author(s): Jovent Muliadi ; Axel Azriel

- Foreign recorded two years of consecutive outflows and still continue on YTD basis. We expect the flow to turnaround amid EPS inflection.

- We expect stocks under our coverage to book 10% EPS growth in FY26F (+15% for IDX80), after booking -3% EPS growth in FY25.

- We view fiscal as the key risk, stemming from large revenue shortfall and elevated spending that could lead to higher bond issuance/wider deficit.

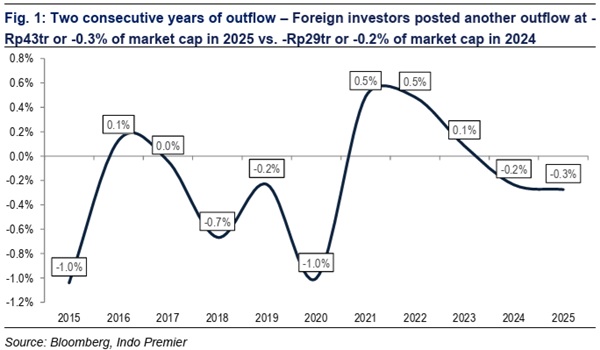

Consistent outflow in the past 2 years

Foreign has booked -Rp43tr outflow in JCI (-Rp46tr in IDX80) in 2025 and continuation post -Rp29tr outflow in 2024 (-37.3tr in IDX80) - this represents -0.3/-0.2% of market cap in 2025/24. This was similar to 2018-2020 period where foreign booked a total -Rp123tr of outflow (-Rp61/17/46tr in 2020/19/18 or -1.0/-0.2/-0.7% of market cap). We believe the outflow in 2025 was expected as JCI booked -7% EPS growth (our coverage at -3% yoy) along with the change in political landscape. However, the outflow continues YTD with -Rp17.3tr, with banks remained the biggest source of outflow especially at -Rp15.9tr YTD (-Rp28.8tr in 2025) amidst non-fundamental concern and was exacerbated by recent event on Martabe (); this was despite 's strong fundamental.

Earnings inflection should be the main catalyst

After posting -3% EPS growth in 2025, we expect stocks under coverage to book 10% earnings growth whereas IDX80 is projected to generate 15% EPS growth. With bulk of the earnings recovery shall come from: metals and oil & gas. However, we think there is a good chance that consensus also underestimated banks' earnings estimates at 6% i.e. booked 16% earnings growth in Jan26. Note that post announcement of 's 4Q25 result (which was a beat), experienced sizable foreign inflow of +Rp2.8tr vs. its big 3 peers of +Rp1.2tr/-Rp58.6bn/-Rp4.4tr for /BBNI/BBCA (during 6th Feb26 to 26th Feb26).

Fiscal may be the biggest risk for 2026

Given that there is a big shortfall in revenue of Rp248.8tr in 2025 (91.7% of 2025's target which translate in -3.3% yoy drop in revenue) from the miss in tax collection; and higher revenue target of +14.4% yoy in 2026, we expect that there is a good chance that overall revenue might miss again this year. At the same time, overall spending increases by +11.3% yoy - largely coming from nutritious meal program (to Rp335tr from Rp51.5tr or +550.5% yoy) and defence spending (to Rp337.4tr from Rp166.2tr or +103.0% yoy); worth noting that some of the spending also been shifted to SOE banks i.e. village cooperatives. This creates a risk in overall fiscal position and may result in either higher financing needs (also deficit) and/or curb in spending. Further implication of fiscal risk is rating downgrade by Fitch/Moody's and S&P, ultimately translate to even higher cost of borrowing and financing needs.

We prefer commodity space and companies with strong earnings growth

Given the fiscal risk and current geopolitical condition, we prefer commodities names such as: , , and Merdeka group. We also like companies with strong earnings recovery i.e. /BRIS/BBTN. JCI/IDX 80 currently trades at 15.5x/12.6x FY26F P/E vs. its 10Y average of 16.7x/14.0x (5Y for IDX80 as it was launched in Feb2019), which is really attractive, in our view. Another risk is liquidity for banks especially in 2Q during dividend period.

Sumber : IPS