Company Update / Coal / IJ / Click here for full PDF version

Author(s): Reggie Parengkuan ;Ryan Winipta

- Komatsu and Pama volumes declined by -58/-12% mom in Feb26 amid RKAB issue and Ramadhan seasonality.

- TTA's RKAB was cut by 50% compared to its proposed target, while Martabe still awaits an environmental audit.

- Maintain our earnings estimates for now; reiterate Hold with an unchanged SOTP -based TP of Rp28,500/share.

Soft Komatsu demand across sectors; 2M26 in-line

Komatsu sales sharply declined to 259 units in Feb26 (-40% yoy/-58% mom), driven by lower demand across sectors (mining -51%/forestry -89%/construction -50%/agro -35% mom). Mining and forestry demand were particularly soft due to RKAB issue and Ramadhan seasonality. Nonetheless, 2M26 sales volume of 869 units (-11% yoy) remained in-line with 's FY26F guidance of 4,500 units (at 19% vs. 5yr avg of 17%).

Pama volumes declined but remained in-line with guidance

Pama coal production and OB volume declined to 9.6Mt/74.3mbcm in Feb26 (-10/-12% mom), likely due to higher rainfall and continued cost efficiency measures by miners. Overall, 2M26 coal production/OB volume of 20Mt/159mbcm (-7/-7% yoy) was in-line with 's FY26F guidance (at 14% vs. 5yr avg of 14%).

Soft TTA coal sales on logistical issue; RKAB cut 50%

TTA coal sales was also soft in Feb26 (1.3Mt; -15% mom), driven by both lower thermal and coking coal sales of 1.1Mt/202kt (-9/-35% mom). As a result, 2M26 thermal/coking sales volume of 2.3/0.5Mt (+10/-36% yoy) came in below 's FY26F guidance (at 17/10% vs. 5yr avg of 22%). Note that TTA has been approved for 7.5Mt RKAB in FY26F, 50% lower compared to initial guidance of 15Mt, but revision in 2H remains possible.

Gold sales was flattish as Martabe still awaits environmental audit

Gold sales volume remained flat mom at 1koz in Feb26, bringing 2M26 sales volume to 2koz (-95% yoy; at 1% FY26F guidance). Martabe is currently awaiting an environmental audit to commence and expects operations to resume 2 months thereafter.

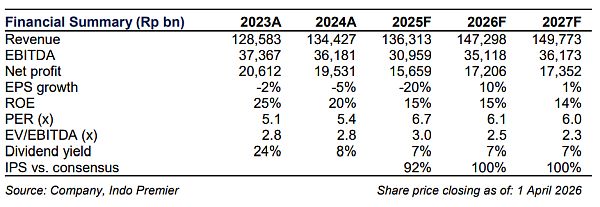

Reiterate Hold at unchanged SOTP -based TP of Rp27,000/share

At the current run rate and excluding potential losses in mineral mining (gold & nickel), we expect to record Rp3.2tr NP in 1Q26F. We maintain our NP estimates for now and reiterate our Hold rating with an unchanged TP of 28,500. Key catalysts include the resumption of Martabe operations and looser RKAB approval. To add, has extended its Rp2tr buyback program up until 30Jun (from 15Apr).

Sumber : IPS