Company Update / Banks / IJ / Click here for full PDF version

Author(s): Jovent Muliadi ;Axel Azriel

- 1Q26 net profit of Rp15.4tr (+17% yoy) was a beat. PPOP was robust (+10% yoy) from solid NII; CoC of 58bp at lower end of guidance.

- NIM fell -5bp yoy to 4.7% in 1Q26 amid lower loan yield though was offset by CoF. Loan grew robust (+16% yoy) from corporate and commercial.

- LAR improved to 6% in 1Q26 vs. 7.2% in 1Q25 along with stable NPL. remains our top pick amid robust PPOP and resilient asset quality.

1Q26 results: beat amid solid PPOP /NII and lower CoC

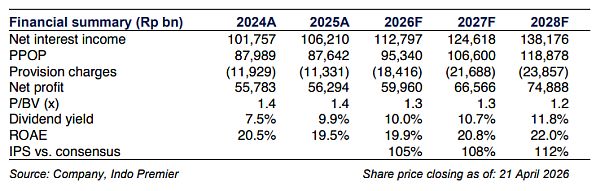

net profit of Rp15.4tr in 1Q26 (+17% yoy) was a beat against ours/consensus FY26F estimates at 26/27% - note that consensus only expect +2% yoy earnings growth for FY26F. PPOP came robust (+10% yoy) from solid NII (+11% yoy) and manageable opex (+7% yoy) while non-II came softer (+5% yoy - primarily weighed down by lower recovery of -40% yoy). Provision eased -20% yoy which translates to lower CoC of 58bp (-25bp yoy), at lower end of its FY26F guidance of 60-80bp.

Relatively stable NIM as drop in loan yield was offset by improving CoF

Consolidated NIM eased -5bp yoy to 4.7% in 1Q26, driven by lower loan yield (-53bp yoy) mainly from declining reference rate within the wholesale segment. On a more positive note, CoF has already improved by -42bp yoy. Deposit grew +21% yoy with TD surging +45% yoy while came at +13% yoy (CA rose +20% yoy vs. SA of +6% yoy). LDR stood at 91% (vs. 94% in 1Q25). revised its FY26F NIM guidance to 4.5-4.7% (vs. 4.6-4.8% initially), primarily due to BSI deconsolidation adjustment & lower loan yield assumption.

Strong loan growth still supported by corporate and commercial

Loan growth of +16% yoy (+2% qoq) came above its FY26F guidance of 7-9%. It was led by corporate (+29% yoy) driven by Agrinas loans, followed by commercial (+13% yoy). Micro & payroll grew +3% yoy while consumer remained slow at +2% yoy.

Resilient asset quality especially on LAR

LAR improved to 6.0% in 1Q26 (vs. 7.2% in 1Q25), along with stable NPL at 1.0% (flat yoy). LAR coverage declined to 40% vs. 43% in1Q25. Recovery/write-off ratio reached 80% in 1Q26 (vs. 104% in 1Q25), with write offs at Rp1.3tr in 1Q26 (-20% yoy) vs. Rp1.6tr in 1Q25, suggesting continuous improvement in asset quality.

remains our top pick amid robust PPOP and resilient asset quality

We maintain our Buy rating on. It remains our top pick amid strong PPOP performance and resilient asset quality especially on LAR. currently trades at attractive valuation of 1.2x P/B and 7.3x FY26F P/E (vs. 10Y avg. of 1.6x P/B and 11.3x P/E).Risks are slower loan growth and NIM compression.

Sumber : IPS